My High School Final Paper

My Class of 2025 High School Final Paper

As the title says, below is my high school Final Paper that I wrote partly in 2024 and partly in 2025 before graduating high school in the summer of 2025. It is probably not super interesting to veteran traders as its purpose was to explain these topics to a layman and certain concepts are oversimplified. Nevertheless, I think it might still be interesting to some and offers a handful interesting trades that I have taken in the past. If you’d like to skip to these, they are under chapter 4. Trade 4.2 is a personal favourite of mine.

1. Personal Introduction

Like many young people at the age of fifteen, I was unhappy with my situation. I was not a fan of school and felt like I did not have much going for me. I was bored and needed to find something to keep me occupied and help me elevate in life.

At the time, trading was very popular. Like many teenagers, I fell for the pipe dream of ‘price action’ trading – the idea that you can easily make quick money from trading by drawing support and resistance lines on asset charts. Since this trading style was rumored to work on all assets, I chose crypto since it had lower fees and was more volatile.1

In hindsight, I can say with confidence that it was nothing more than a waste of time. After almost two years of trying to make this form of trading work, I finally realized that it was mostly a scam and quit.

In the spring of 2023, I switched to a new trading style with around 300 Dollars left in my account. I began looking for opportunities to make money without drawing lines on charts, instead focusing on news and narratives. One of my first trades was shorting2 Dogecoin after Elon Musk’s SpaceX rocket exploded. This type of trading clicked for me immediately, and I was profitable from the start. I made a conscious decision to stick with crypto trading, since it seemed easier at the time and offered more opportunities, such as my Dogecoin trade, compared to other markets.

I kept on trading the bear market3 of 2023, compounding wins and growing my account value. However, in August 2023, I took a big hit by taking on too much risk and lost most of what I had worked for, leaving me back at 300 Dollars.

In September 2023, I started networking on Twitter and formed my own trading group to discuss trades and strategies with other like-minded people. I made great friendships along the way and connected with some of the best traders. By the end of 2023, the bear market was over, and it was clear to me that another big bull market4 had started. I had to change my trading style, focusing more on longing5 rather than shorting.

Despite my major progress, I faced another big loss in April 2024, again by taking on too much risk. I lost over 70% of my money. The emotional hit was massive, however, it once again taught me the importance of good risk management. It took countless small, compounded wins to make it all back, especially since between April and October 2024, markets were going sideways and conditions were rather dry, but I managed to do it.

Since then, I have traded every day, putting thousands of hours into perfecting my craft. Now, I have achieved over a 15’000% return on my initial investment. However, I am far from satisfied and will keep on trading for as long as market conditions allow me to be profitable.

The more time I have spent in crypto, the more I have realized what a rare opportunity it is to earn such great returns as a lone retail trader6 and that this would not be possible in other financial markets.

In this paper, I aim to share why trading crypto is more lucrative, and quite frankly, easier than trading other markets like the stock market, and provide opinions on why that is the case.

2. Efficiency

2.1 The Definition of Market Efficiency

Since this paper is based on the inefficiencies of the crypto market, it first has to be made clear what it actually means if a market is efficient or otherwise inefficient.

Simply, market efficiency is defined as the following:

“Market efficiency refers to the degree to which market prices reflect all available, relevant information.” (Investopedia, 2022)iii

“If market prices are efficient, then all information is already incorporated into prices, and so there is no way to ‘beat’ the market because there are no undervalued or overvalued securities available.” (Investopedia, 2022)iii

Essentially, this means that if a profitable trade idea, or inefficiency, presents itself, market participants will immediately take that trade with the goal of making profits. Since market prices are primarily driven by the actions of traders, these traders will fix the inefficiency, making the market efficient again. Therefore, in an efficient market, it should theoretically not be possible to earn money from trading at all.

2.2 Earnings Reports Efficiency

The easiest way to demonstrate what efficiency in a market looks like is by looking at news trades. Each quarter, public companies release their earnings statements. Since stock prices reflect the expected value of a company, if a company reports higher earnings than expected in such an earnings report, its stock price should increase. Therefore, if a company ‘beats’ its expected earnings, a logical trade idea would be to buy the stock of said company after the news is released. However, in an efficient market, it should not be possible for most investors to earn a profit from such a trade.

The research report by the Journal of Accounting Research, titled “How is Earnings News Transmitted to Stock Prices” examines the speed and mechanism of the price discovery following earnings announcements. (Journal of Accounting Research, 2022)iv

Simplifying their findings on how quickly individual stock prices react to earnings announcements, it gives us the following table:

Figure 2: Findings on the speed at which earnings reports are priced in; (compiled by ChatGPT)

The authors of the research report used a sample size of 8’964 earnings announcements of companies in the S&P 500 index during the period from January 1, 2011, to December 31, 2015. By utilizing high-frequency trade and quote data from NASDAQ Totalview-ITCH and Thomson Reuters Tick History, which provide timestamps in the milliseconds, they found that following the earnings announcements where companies either exceeded expected earnings or fell short of expected earnings, their stock’s Best Quote return changed by an average of 3.25%, either up or down, within milliseconds. The Best Quote return can simply be defined as the new price of the stock, even if no trades have been executed since the earnings report was released. What this means is that the price of the stock has adjusted to the new earnings in a matter of milliseconds, leaving market participants no time to trade based on the earnings report. This accurately demonstrates what an efficient market looks like. Furthermore, what the study found is that after the release of these earnings reports, no trades were executed, but the price of the stock still changed based on the new earnings. This is because the market maker7 immediately adjusted their bids and asks8 based on the new earnings.

2.3 Zero-Sum Nature of Financial Markets

Markets are player-versus-player environments. They have a zero-sum nature. This means that if one person makes a profit in the markets, another has to lose. Say unexpected positive news for a company is released – perhaps they just announced a new promising product launch. Market participants who see this news will want to buy the company’s stock because they expect its value to rise. But since markets are a zero-sum game, only the traders who react the quickest will make a profit. This is because in order for you to buy the stock, someone else has to sell it to you. The fastest traders get in at a lower price before the stock has fully reacted to the news. Once they have bought the stock and the price rises as more people buy the stock based on the news, these fast traders sell the stock at a profit. In order for them to sell the stock, someone else has to buy it from them. Most of the time, they sell it to slower traders who are also trying to buy based on the same news. However, by the time these slower traders enter, the price has already risen, and they are now paying a higher price. The quickest traders have already locked in their profits and exited, leaving the slower ones ‘holding the bag’ at a price that may not rise further, or may even fall back down. The faster traders directly profit from those who were slow to act on the same news.

How efficient a market is is often determined by the degree of competition that exists within it.

In this example, the degree of competition, or how fast these faster traders truly are, determines how difficult it is to profit from such a situation.

Speed is perhaps one of the most important prerequisites in order to gain profits in the financial markets through trading. In traditional financial markets, unexpected news is priced in within milliseconds most of the time, leaving most traders unable to profit. This is because the degree of competition is incredibly high. Those ‘faster traders’ that are able to profit are often massive firms, hedge funds, and even banks with thousands of traders and billions in capital. Oftentimes, they do not even manually trade such events but instead use trading bots that can trade based on news within milliseconds. The competition is so strong that certain trading firms even set up servers close to stock exchanges in order to reduce the time it takes for their orders to reach the exchange. Since proximity reduces latency, being closer to a stock exchange means that your servers can send and receive trading orders faster than competitors further away. In another example, Jump Trading, a trading firm, installed a private optical fiber cable under an Ohio field to reduce latency between the Chicago Mercantile Exchange and the New York Stock Exchange in order to achieve milliseconds or even microseconds of speed advantage over competitors by reducing the physical distance that data signals need to travel. (Financial Times, 2024)v

The cost of such a cable is in the tens of millions, which shows how far trading firms will go to beat their competitors. This illustrates that it is basically impossible for a lone trader who trades from their home computer to beat this competition.

2.4 Conclusion on Market Efficiency

In conclusion, trading traditional markets such as the stock market is much more difficult because of the competition consisting of such professional players. However, crypto traders have long known that trading crypto is much easier, since not many trading firms have entered the crypto space, making it easier to profit from trades such as news trades because your competition mainly consists of other traders who are trading from their home computers and are much slower than a professional trading firm would be. In the following chapters, we want to take a detailed look at strategies and trades that prove that the crypto markets are, or at least were, quite inefficient.

3. Crypto Trading Strategies

3.1 News Trading

3.1.1 Introduction

Since a good way to measure how efficient a market is, is by how quickly news is priced in9, in inefficient markets it usually takes longer for news to affect prices.

As we have seen, in traditional markets such as the stock market, news such as earnings reports is priced in almost instantly, without allowing traders a chance to profit. However, in the crypto markets, this is often not the case and it takes longer for market prices, driven by traders, to react.

3.1.2 Example

One great recent example that demonstrates this fact was an impactful news release surrounding the potential approval of an Ethereum ETF.10

In January 2024, the SEC, the U.S. government agency that regulates financial markets, approved a Spot Bitcoin ETF, allowing investors to buy Bitcoin more easily, directly on the stock market without having to buy it on crypto exchanges. This was an important occurrence and resulted in billions of dollars worth of buying pressure, leading to a heavy price increase in Bitcoin.

Following Bitcoin’s ETF approval, asset management companies such as BlackRock filed for a Spot Ethereum ETF with the SEC, meaning the SEC would still have to approve the ETF before it could start trading. Since Bitcoin’s price increased strongly following its ETF approval, market participants expected the same thing to happen to Ethereum if the Ethereum ETF were to be approved.

The SEC’s deadline for either approving or denying the Ethereum ETF was set for the end of May 2024. However, the general consensus was that the SEC would deny it, based on expert opinions and research reports. What this means is that a denial of the ETF was already priced in. Therefore, if the ETF were denied as expected, Ethereum’s price would likely not move much. Conversely, if it were approved, its price would increase heavily since traders were hoping for the same run-up in price that occurred after Bitcoin’s ETF approval.

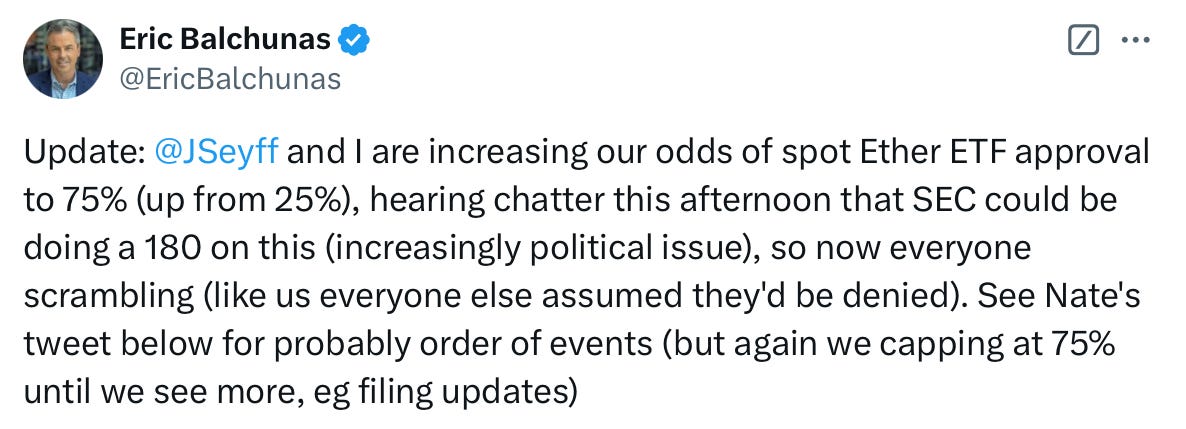

Unexpectedly, the two leading ETF experts, who had initially stated that they believed the ETF would be denied, changed their opinion, expressing that they now believe in an approval of the ETF.

Figure 3: Eric Balchunas tweet on ETF approval odds; (Twitter)

Nobody had expected such a high chance of an approval, meaning the market was wrong and Ethereum’s value was too low. Since a likely ETF approval was not reflected in its price, Ethereum should be bought.

Figure 4: Ethereum Price Action following Eric Balchunas tweet; (treeofalpha.com)

The chart above displays the price of Ethereum following the tweet by the ETF expert Eric Balchunas on increasing their odds of an Ethereum ETF approval. The exact timestamp at which the tweet by Eric Balchunas was posted is marked by the ‘Timestamp’ symbol. Each candle displays exactly one minute of price action. The chart indicates that it took several minutes for market participants to react to the news by buying Ethereum. This clearly shows the delay in the market’s response. Even without the best and fastest infrastructure and tools available, many traders were able to profit by acting on the news.

3.1.3 Explanation

While crypto markets are definitely slower to react to news than traditional markets, most of the time, profiting from news still requires more than just being aware of it and buying Ethereum based on good news, for example. Instead, crypto news trading does still require the right skills and tools to become profitable. In crypto, there is a large community of specialized news traders who focus exclusively on trading news and nothing else. One such trader going by the pseudonym ‘WorshipXBT’ has built a reputation on Twitter for making consistent profits from news trading. In fact, it’s his full-time profession, and he relies entirely on trading news to earn an income.

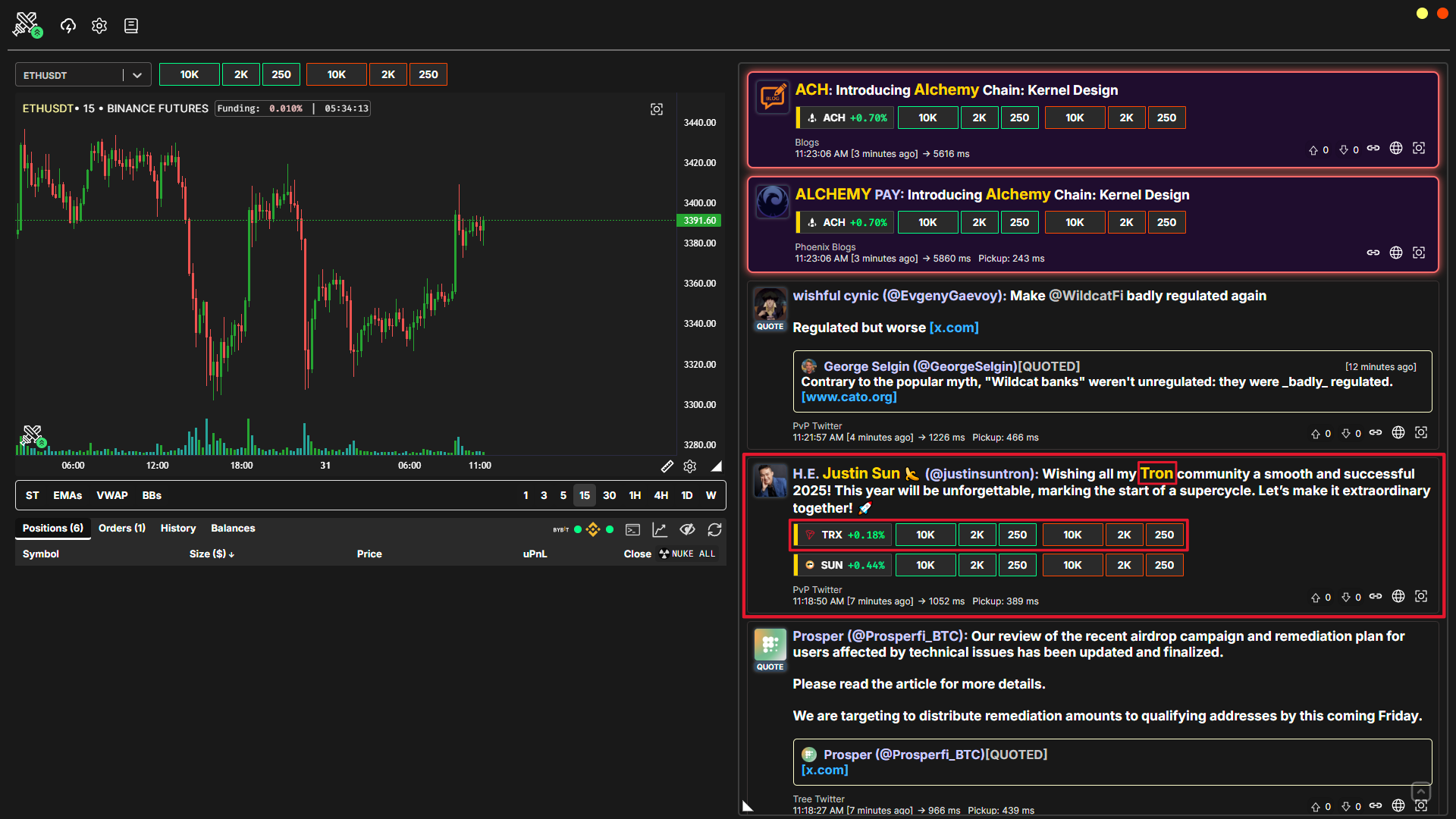

In order to gain a speed advantage to trade news, he uses a news trading terminal called ‘PVP Terminal.’

Figure 5: PVP Terminal Desktop Application; (Screenshot, 2024)

The above image is a screenshot of the PVP News Trading Terminal. The left column displays a chart and below the trader’s open positions. The news feed is in the right column. It picks up news in the form of web blogs, Telegram messages, and Twitter posts related to crypto and forwards them to the terminal.

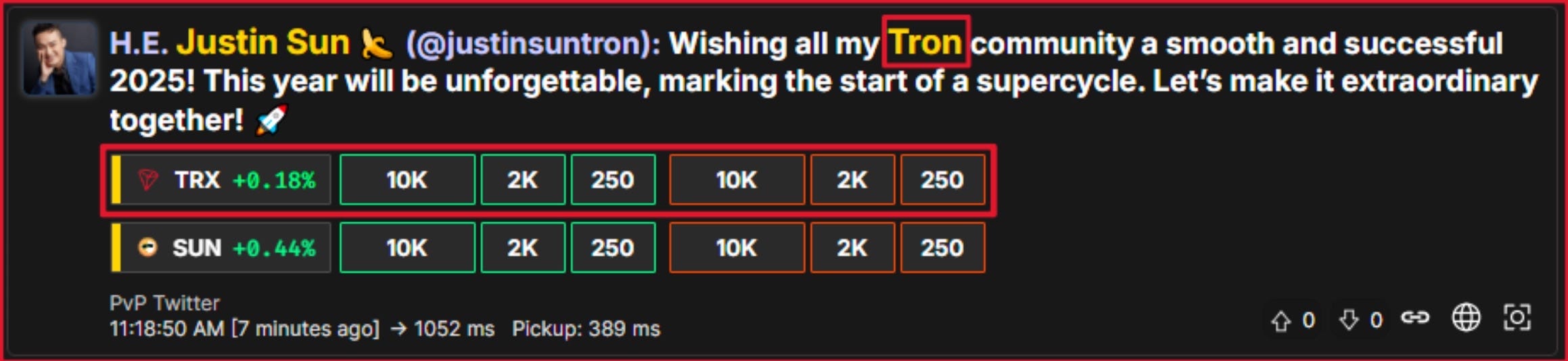

Figure 6: PVP Terminal Justin Sun forwarded tweet; (Screenshot)

The highlighted message is a forwarded tweet by Justin Sun, a prominent crypto founder. The terminal scans the message and picks up the word ‘Tron’, which is a cryptocurrency with the ticker symbol $TRX. Because Tron is in the message, the terminal automatically displays trade buttons in order to trade Tron with predetermined position sizes which are customizable. With these trade buttons, the trader can instantly open a short or long position in just one click, which offers an incredible speed advantage compared to if he had to manually search for the ticker, input the position size, and open a position.

WorshipXBT takes news trades based on experience of what can cause a cryptocurrency to react to a certain piece of news. Good examples are SEC lawsuits. If the SEC sues a company that has a token, he shorts their token. On the other hand, if a protocol proposes a fee switch11, he longs their token.

What makes a great news trade is composed of two factors:

Correct interpretation of news

Speed

Firstly, the news trader has to read the piece of news and correctly interpret it. He has to decide whether it is impactful, meaning if it will cause a move in the concerned token’s price. Moreover, he has to conclude in which direction this price move will occur. If the news is negative, he shorts the token, making money when it goes down in value. If the news is positive, he longs the token, making money when it goes up in value. After deciding whether or not he should open a long or short position, he has to quickly enter the trade, ideally before most other traders do. If he is slow and most traders have already bought on positive news, the token has already moved up in value, and he is too late, buying after the news is already priced in.

Less impactful news, unlike the Ethereum ETF approval news, is more difficult to trade and are priced in more quickly. For WorshipXBT, it takes around two to three seconds to enter a trade after receiving news, leaving little time to think much.

“We are trading in 2-3 seconds so thinking isn’t really a thing, mostly just reactions based on experience.” -WorshipXBT (WorshipXBT Interview)vi

3.1.4 Evolution

While it is still possible to earn a consistent living from crypto news trading as WorshipXBT does, he states that it has definitely gotten harder than when he first started news trading in 2023. This can mostly be attributed to a higher level of competition. Since news trading was so lucrative, more traders have joined the news trading space using the same tools, such as terminals. Furthermore, there has been an increase in sophisticated traders using bots to trade. A news trading bot can for example pick up the words “SEC sues” + “the token” and automatically short said token, entering the trade before manual traders who then get in at a lower, less favorable price.

“There were certain types of news you could trade manually that have now become ‘solved’ by botters. Things that are predictable or standardized which can be botted have largely been solved. However, the most ‘juicy’ news is unpredictable by definition and there is still a lot of money to be made there.” -Dipper, professional crypto trader (Dipper Interview)vii

3.1.5 Personal Conclusion

The fact that news trading has gotten more difficult accurately highlights the path most profitable trading strategies take. As more traders realize a strategy is lucrative, they start trading it too, leading to more competition, and in the worst cases, reaching such a high state of competition that the strategy is no longer profitable for most traders. The market has gotten more efficient.

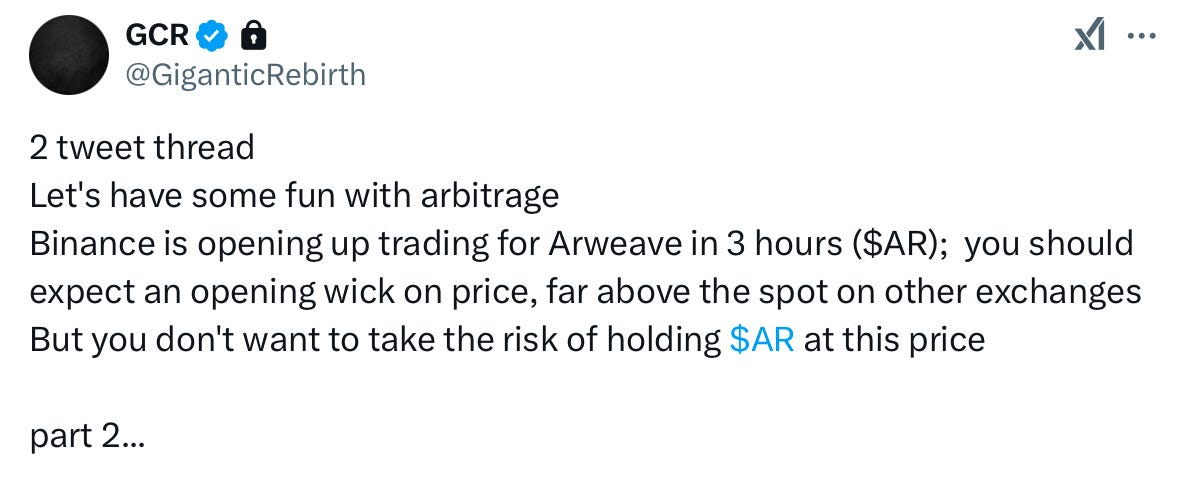

3.2 Exchange Listing Arbitrage

3.2.1 Introduction

Going through a trader’s old Twitter posts, one could find an incredibly profitable, near zero-risk strategy.

Figure 7: GCR Twitter post on exchange listing arbitrage part 1; (Twitter)

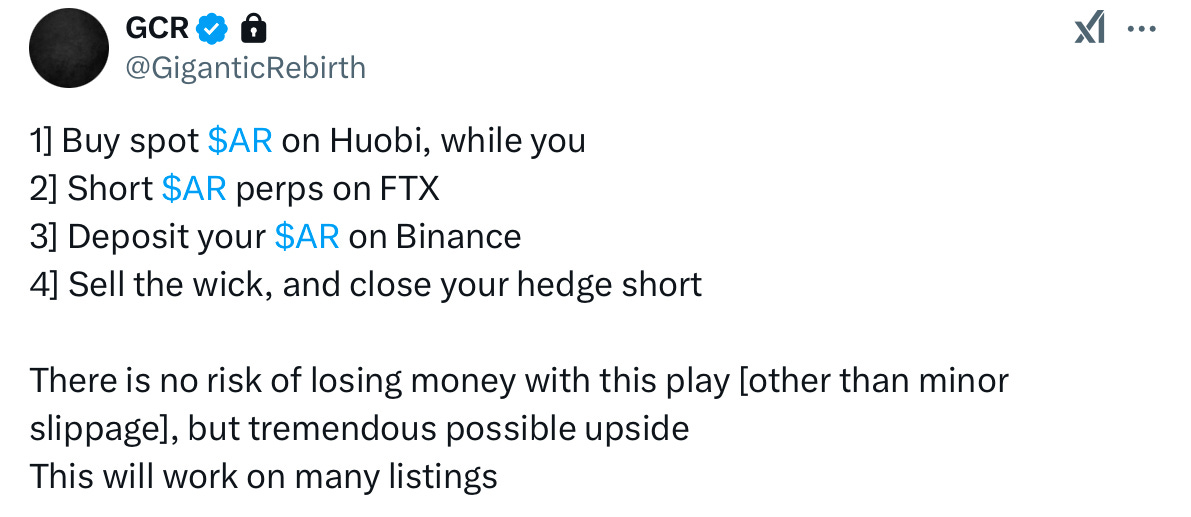

Figure 8: GCR Twitter post on exchange listing arbitrage part 2; (Twitter)

3.2.2 Explanation

Explained above is an exotic arbitrage12 strategy – profiting from price differences in the same token across exchanges. To buy a token on one exchange and sell it on another for a higher price is a plain vanilla arbitrage strategy. The reason this strategy mentioned above is considered exotic, is since it is slightly more complex and takes advantage of an anomaly persisting in the crypto markets. Unlike the stock market, where stocks are normally traded solely on one exchange, for example, the New York Stock Exchange, in crypto, tokens are traded on each exchange individually. The prices are typically kept the same through traders conducting plain arbitrage trades. However, when tokens are listed on a new exchange, they often reach much higher prices in the first few seconds of trading than on the exchanges where they were already trading.

In the example explained by GCR, Binance planned to list $AR on May 14, 2021. $AR was already being traded on other exchanges prior to its Binance listing. It was expected that the price of $AR would spike above its price on other exchanges, as had previously happened with other listings, thereby creating an arbitrage opportunity. In the case of $AR, it reached a price of 77.60 Dollars on Binance compared to 44.00 Dollars on other exchanges – a price difference of 77%.

3.2.3 Example

In order to profit from this price difference, the strategy laid out is rather simple: Buy $AR on an exchange where it is already being traded, such as Huobi, and at the same time, short $AR through a futures contract.13 This way, you are protected against any moves in the price of $AR that might occur before you can sell it once it is listed on Binance, since for every dollar that your purchased $AR tokens might move down in value, you would gain a Dollar from your short position.

Let us say you bought 1’000 $AR tokens on Huobi and shorted 1000 $AR contracts both at an average price of 44.71 Dollars. You then send these 1000 tokens to Binance. Once trading for $AR opens on Binance, you sell all 1’000 tokens and close your protective futures contract short position simultaneously. While $AR did reach a highest price of 77.60 Dollars on Binance, realistically, your sell orders will not get executed at the highest possible price due to low liquidity.14

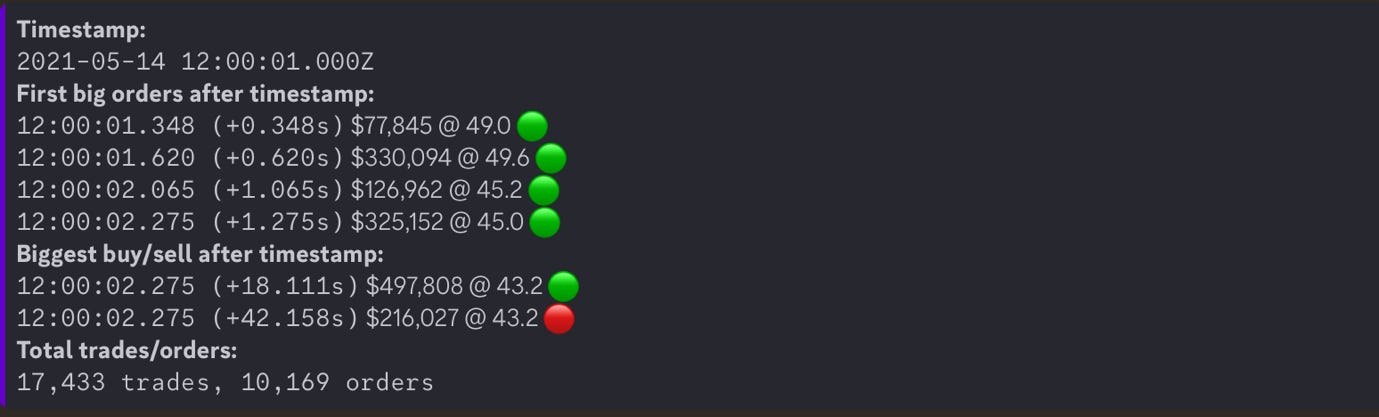

The figures below display all $AR trades executed on Binance in the two minutes following its Binance listing.

Figure 9: Executed $AR trades on Binance, after its listing; (sadward chartbot 2)

Figure 10: Executed $AR trades on Binance, after its listing; (sadward chartbot 2)

Looking at these executed trades, barely any orders were filled above 50 Dollars per $AR. However, there were multiple large orders filled above the price traded on other exchanges, which was around 44 Dollars at the time of the Binance listing. The highest order was filled for 330’094 Dollars at 49.00 Dollars per token, a price difference of 5 Dollars per AR.

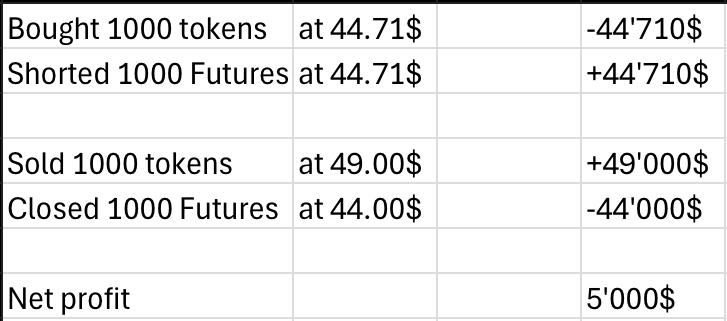

The 1’000 tokens you bought at 44.71 Dollars per token for 44’710 Dollars were now sold at 49 Dollars per token for 49’000 Dollars, a profit of 4’290 Dollars.

Since the value of $AR on other exchanges dropped from 44.71 Dollars when you purchased them to 44 Dollars at the time of the listing, including the futures contract, you have also profited 0.71 Dollars per futures contract, which you shorted as a protective position, generating another 710 Dollars in profits. Transaction and transfer fees are so low they can be disregarded.

Figure 11: Hypothetical trades for $AR exchange listing arbitrage; (Excel)

This brings the total profit of this hypothetical trade to 5’000 Dollars – a trade that only lasted a few minutes and carried no directional risk.

3.2.4 Evolution

Next, we want to look at how this strategy has changed over time. We will analyze Binance listings from May 2021 to October 2024.

Namely, $JASMY (November, 2021), $KDA (March, 2022), $GMX (October, 2022),

$GNS (February, 2023), $SYN (February, 2023), $PEPE (May, 2023), $FLOKI (May, 2023), $WIF (March, 2024), and $BOME (March, 2024).

Figure 12: Price differences across exchanges in tokens after Binance listing; (Excel)

While $JASMY, $KDA, and $GMX all offered highly profitable trade returns using this strategy, since the listing of $GMX in October 2022, no other new listings, including but not limited to $GNS, $SYN, $PEPE, $FLOKI, $WIF and $BOME, have risen above prices in the first few minutes of being listed on Binance, compared to other exchanges.

The rapid shift from a 30 Dollar price difference to no difference at all between the listings of $GMX in October of 2022 and $SYN in February 2023 may indicate that a single entity, either a very large trader or perhaps a fund, has become aware of this strategy. Inevitably, by trading it with large amounts of capital, they have eradicated this edge. This is what we call a ‘decayed edge’.

3.2.5 Personal Conclusion

This strategy, while it was still effective, was very successful, mainly because there was almost no risk involved. Even if the price of the token you wanted to sell at the time of its listing did not rise above that on other exchanges, you would not have incurred any losses aside from minimal transaction fees, since you were protected via a futures contract. This edge therefore offered very high potential rewards, all in just a few minutes of trading and with very limited downside.

3.3 MEV bots

3.3.1 Introduction

A trading style that has seen a significant rise in popularity since 2023, which also became a hot topic due to its high profitability matched with almost no risks, and furthermore, its unethical tendencies, is the usage of MEV bots.

“MEV is basically the extraction of value from the inefficiencies in the market, whether it be from price discrepancies or user tolerance. On Ethereum this is done generally by searching for value through ordering transactions in such a way to maximize the value captured by both yourself and the network” -jaredfromsubway (Cryptic Woods jaredfromsubway Interview)x

3.2.2 Explanation

While this sounds very complicated, it is easier to understand than it first seems. One strategy MEV bots use is called a sandwich attack. Sandwich attacks involve two transactions that ‘sandwich’ a victim’s trade: One transaction is executed before the victim’s trade, and another is executed immediately after. The goal is to profit at the expense of the unsuspecting trader. (Trust Wallet blog)xi Jared gives us an analogy to understand what is exactly meant by this, and how the MEV user profits from a sandwich attack. Imagine someone posts on a marketplace that they are willing to buy Taylor Swift tickets for 10’000 Dollars, even though their retail price is only 5’000 Dollars. To profit from this, a trader would buy them quickly for 5’000 Dollars and sell them to the marketplace buyer at 10’000 Dollars. In the crypto markets, such a trade can occur when a user sets a high slippage15 tolerance before buying a cryptocurrency directly on the blockchain. Most often this is done as a mistake because the user is not aware of slippage tolerances. For example, if a user’s slippage tolerance is set to 10% for buying a token, their trade will execute even if the price that they are paying for the token is 10% higher than the actual market price of said token.

The prerequisites that make this type of sandwich trading possible are only found in the crypto markets:

All transactions on blockchains such as Ethereum are public.

Users can choose to pay a higher gas fee16 in order for their transaction to be executed more quickly.

A MEV bot scans all pending transactions on a blockchain, meaning transactions that are waiting to be executed but have not been confirmed yet. When a MEV bot finds a pending transaction where ‘User A’ is attempting to buy a token with a high slippage tolerance, such as 10%, the bot quickly submits its own transaction to buy that token first. By paying a higher gas fee than User A, the MEV bot ensures that its transaction is executed before User A’s order. This front-running transaction drives up the token’s price. Because this all happens in milliseconds, User A does not have time to cancel their order and is forced to buy the token at a much higher price, since their slippage tolerance allows it. Through User A’s purchase, the price of the token has further increased. Once User A’s transaction is executed, the MEV bot immediately sells its tokens at the inflated price, profiting from the price increase caused by User A’s purchase. As a result, the token’s price quickly drops back to its original level, leaving User A with a loss since they bought the token at an artificially inflated price. The MEV bot profits directly at the expense of User A.

3.2.3 Example

Figure 13: MEV bot sandwich trade example (Dexscreener)

The above figure shows a perfect example of what such a trade looks like. It shows the three transactions involved in a sandwich trade, with the first transaction being at the bottom, and the last at the top.

The MEV bot’s buy transaction (buying 1’420 $wTAO)

The second manual transaction initiated by a human (buying 1’443 $wTAO)

The MEV bot’s sell transaction (selling 1’420 $wTAO)

This incident occurred when a user was trying to buy the token $wTAO on the Ethereum network. The user initiated a buy order for $wTAO while seemingly setting a very high slippage tolerance. The MEV bot immediately detected this pending buy order, and, within milliseconds, submitted its own buy order for the same token with a higher gas fee so that its own order would be executed first. This purchase by the MEV bot caused the token’s price to increase, driving it so high that the user ended up paying almost 527 Dollar per $wTAO, even though the actual market price was only 468 Dollars at the time. Once the user’s transaction executed and further pushed up the price, the MEV bot immediately sold all its tokens at a higher price created by the user’s purchase, leaving the MEV bot with a profit from the difference between its lower initial buy price and the artificially inflated price at which it sold. This sell transaction caused the token’s price to fall back down, consequently leaving the human user with a loss.

3.3.4 Evolution

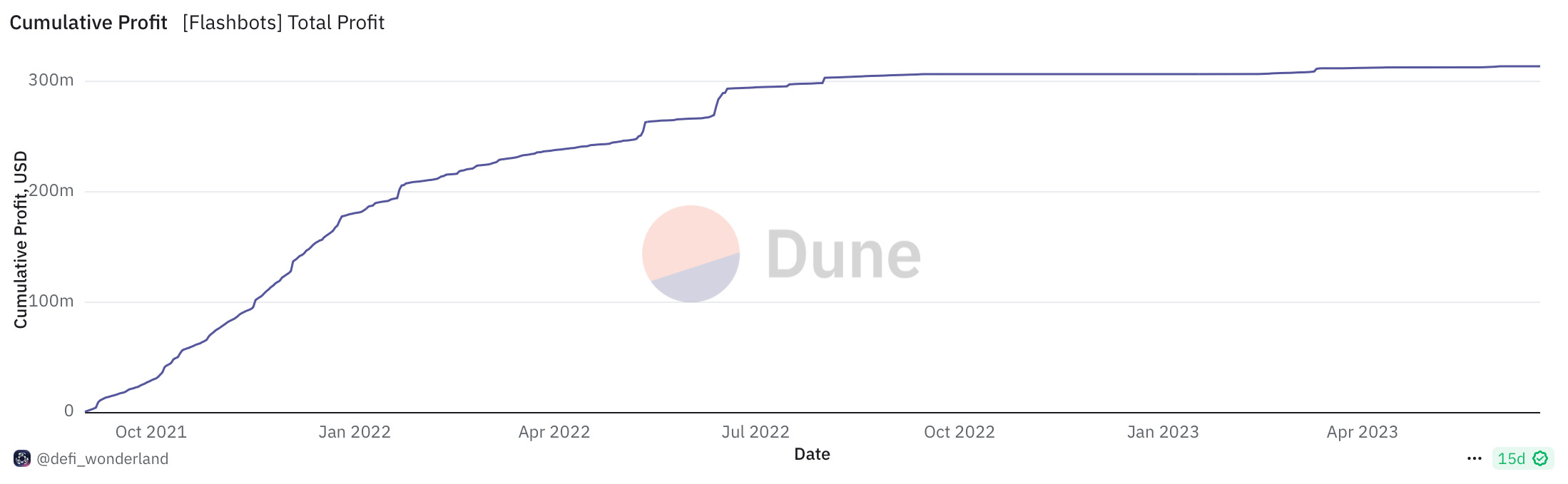

Since MEV bots execute thousands of transactions every day, the best way to measure how their profitability has evolved is by looking at aggregate data of the PNL17 of all MEV bots operating on the Ethereum network.

Figure 14: Aggregate PNL data of Ethereum MEV bots; (Dune)

Above is a PNL chart of all MEV bots operating on Ethereum. Due to the nature of MEV bots, the curve represents a steadily increasing trajectory, since MEV bots are coded so that they only enter a trade that will be profitable. Therefore, if coded right, they never incur any losses.

The key detail to be read from this chart is that MEV bots are making much less profit than they used to in the earlier years. This, like almost all trading strategies, is again attributed to a higher level of competition. Since the number of traders using MEV bots has increased so rapidly, they are competing with one another for sandwich trades. Essentially, MEV bots engage in a gas bidding war, as only the bot willing to pay the highest gas fee has its transaction executed first. This gas fee eats away at profits. However, all trades remain profitable because the MEV bot factors in the gas fees when calculating whether a trade will yield a profit.

3.3.5 Personal Conclusion

MEV bots are an incredibly profitable strategy. If the MEV bot is coded correctly, it will only execute profitable trades, thereby keeping risks very limited. However, the usage of MEV bots is only possible if one has the right coding skills and infrastructure to compete. Profitable bots use complex algorithms to calculate the optimal gas bid. The gas fee needs to be high enough for their transaction to be executed first and low enough so that the trade still yields a profit. Furthermore, a successful MEV bot is highly capital-intensive and requires tools such as private nodes and multiple servers in order to detect trades as quickly as possible. Nonetheless, MEV bots once again teach us how inefficient crypto markets still are. In this case, the inefficiencies that lead to profitable sandwich trades arise because of the high number of unsophisticated traders who are unaware of their slippage tolerance settings.

4. Personal Trades Chapter

In order to gauge what trading inefficient markets like crypto looks like in practice, I will document a handful of additional trades that I have personally taken over the past two years. Furthermore, I will include my own thought process that led to the trade, which is often more difficult than analyzing trades in hindsight.

4.1 AEVO – RBN Arbitrage Trade

4.1.1 Trade Explanation and Thought Process

One interesting trade that highlights how inefficient crypto markets truly are was a conversion arbitrage trade, which yielded a profit of 10% in just 11 days. A conversion of a crypto token happens when a team that is responsible for a pre-existing token, in this case $RBN, decides to re-launch their token and change its name, in this case to $AEVO. These conversions are usually done to give the token a new name, erase old price history, or just bring new attention to the project. Normally, the new token is launched, and on the same day, users who hold the old token can exchange their tokens for the new one, or it is all done automatically. However, in this example, the new token ($AEVO) was launched weeks before the conversion date. Therefore, during the time when the trade took place, both the old token ($RBN) and the new token ($AEVO) existed at the same time and were both tradable.

Figure 15: $RBN to $AEVO conversion guidelines; (Aevo Team website)

As stated on the official website of the token’s team, users will be able to swap $RBN to $AEVO on a 1:1 basis, meaning 1 $RBN can be exchanged for 1 $AEVO.

Figure 16: Inquiry about conversion date; (Aevo Official Discord Server) (I was actually permanently banned from AEVOs Discord after using slurs aimed at the team as a response to them extending their airdrop farming campaign, so thank you to Montag (https://x.com/MontagCapital) for asking for me.) (This detail was not included in the version that I handed in to my teachers)

Furthermore, when asked in the team’s Discord server, team members of Aevo explained that this exchange can be done starting on the 15th of May 2024, 11 days from the time I entered the trade.

Figure 17: grey/white chart $AEVO futures contract price action, red/green chart $RBN price action; (Tradingview)

While looking at the prices of $RBN and the futures contract of $AEVO on the third of May, 11 days before one was able to exchange the two tokens on a 1:1 basis, there was a clear divergence in price between the two assets. Namely, $RBN was trading at 1.20 Dollars and the $AEVO futures contract was trading significantly higher at 1.51 Dollars. $RBN had a discount of about 21% to the $AEVO futures contract. After discovering this fact, the trade idea was simple: Buy $RBN and short the same amount of $AEVO. Since we gain profits if a token that we have shorted goes down in value, if one buys $RBN and shorts the same amount of $AEVO, one is effectively delta-neutral, meaning there is no directional exposure. To clarify, if $RBN and $AEVO both gain one dollar in value, one wins one dollar for every $RBN that one has purchased and loses one dollar for every $AEVO that one is short. This way, you neither make a profit nor a loss. The price action of the two tokens do not matter until the trade is done, when one is able to exchange their $RBN for the same amount of $AEVO, after which the tokens can be sold and the short position closed, yielding a profit of half the price difference between the two assets upon entering the trade, since you don’t only need capital for buying $RBN but also for shorting $AEVO.

However, the trade is not quite that simple, since there are other factors and fees to be taken into account when shorting. Firstly, shorting tokens themselves, such as $AEVO, is not possible. In order to short, one needs derivatives, in this case the $AEVO futures contract. Futures in crypto work differently from traditional finance. In stocks, futures contracts have a settlement date, on which one can exchange their positions for cash, based on the underlying stock at the time of the settlement. This is done to keep the price of the futures contract in line with the underlying stock. In crypto, futures have no expiry date, they are so-called Perpetual Futures. The mechanism that is used to keep the prices of the futures contract and the underlying token at the same level is the presence of funding fees. If a futures contract is trading lower than the underlying token, traders with short positions have to pay fees to traders holding long positions. For the arbitrage trade to work, one has to take these fees into account. In this case, the funding fees for the $AEVO Futures contract were steady at 0%, meaning neither shorts nor longs were being charged. However, these fees can change daily, so they have to be carefully monitored. Next to the funding fees potentially changing to the point of making the trade unprofitable, the biggest risk that would lead to a loss on this trade was the chance of the Aevo team lying about the conversion date or conversion rate. While this possibility seems very small, it is always necessary to consider all possible risks before entering a trade. Based on the history and reputability of the Aevo team, I concluded that the chance of them lying is so minor that one should still take this trade.

4.1.2 Outcome

During the entire duration of the trade, funding fees remained around 0%, therefore having no effect on profits. Furthermore, the Aevo team thankfully kept their promise and allowed $RBN holders to exchange their tokens on a 1:1 basis for $AEVO. As the conversion date arrived, both assets converged to the same price, since traders were now exchanging their $RBN for $AEVO, and I closed the trade at a 10% profit in just 11 days.

4.2 Finding News Early

4.2.1 Explanation and Thought Process

As demonstrated in the News Trading chapter, when trading news, it is important to be faster than the other traders. One needs to enter a trade before the move happens. Normally, market participants receive news at the same time, thereby not giving a single individual a ‘head-start’ to trade off news. However, in this trade example, this is exactly what happened.

In crypto, coins that are backed by teams will often share news on their Twitter account.

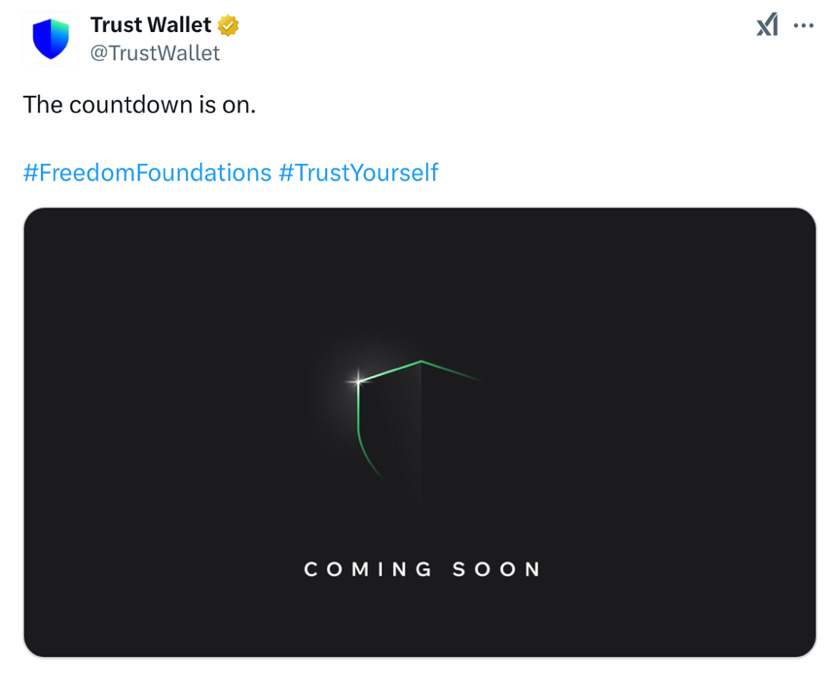

Here, the team behind the $TWT token, called Trust Wallet, posted about an upcoming news announcement, however not revealing what said announcement would be:

Figure 18: Trust Wallet “Coming Soon” Tweet; (Twitter)

This announcement of an announcement was posted on October 4th, 2023.

Figure 19: $TWT October Price Action; (Tradingview)

As seen in the above chart, traders would buy $TWT following the first announcement, speculating on what the final announcement was going to be. Therefore, expectations were quite high, and traders were hoping to receive good news. Knowing that the importance of the announcement was going to be crucial for $TWT’s price, my team and I were searching for a possible way to get the eventual announcement ahead of the majority of traders, and we were successful in doing so. We were able to find out that the Trust Wallet team did not only post from their main Twitter account ‘@TrustWallet’, but also from 7 other accounts that would post the same messages but in other languages. The most crucial fact that we found was that not all accounts would post at the same time – some would post a few minutes earlier or later than the main account. So, we simply monitored all 8 Trust Wallet accounts for days, hoping for one of them to post before the main account. And after 12 days of watching all accounts, our determination finally paid off. On October 16th, at 13:57, the Russian Trust Wallet account (@TrustWallet_ru) posted what we were waiting for.

Figure 20: Twitter Post by Russian Trust Wallet Account; (Twitter)

One of our team members quickly saw the message and notified the rest of us. Trust Wallet announced a new app update, yet no major changes that traders were hoping for. We quickly realized that this announcement did not at all live up to the expectations set by the team and traders. We also knew that there was not much time left until the main Trust Wallet account would post the same announcement, and the rest of the world would wake up to the fact that this announcement was severely underwhelming. So, we began shorting before the market had started moving, since indeed barely anyone else seemed to have caught wind of the announcement.

4.2.2 Outcome

Two minutes after we had picked up the post of the Russian account, the main account posted the exact same message in English, after which the price of $TWT started cratering.

Figure 21: $TWT Price Action following Tweet by Russian Trust Wallet account; (treeofalpha.com)

As seen in the above chart, the orange dot labeled “Timestamp” was the exact time the first announcement was posted by the Russian account. Despite the whole ordeal being hectic, we still managed to open short positions before the market started moving, which we then rode into big profits as the market started selling off based on the main account’s announcement.

Once other traders had seen the announcement and reacted to it, we closed our shorts at a profit.

4.3 Speculating on an Upcoming Token Listing

4.3.1 Explanation and Thought Process

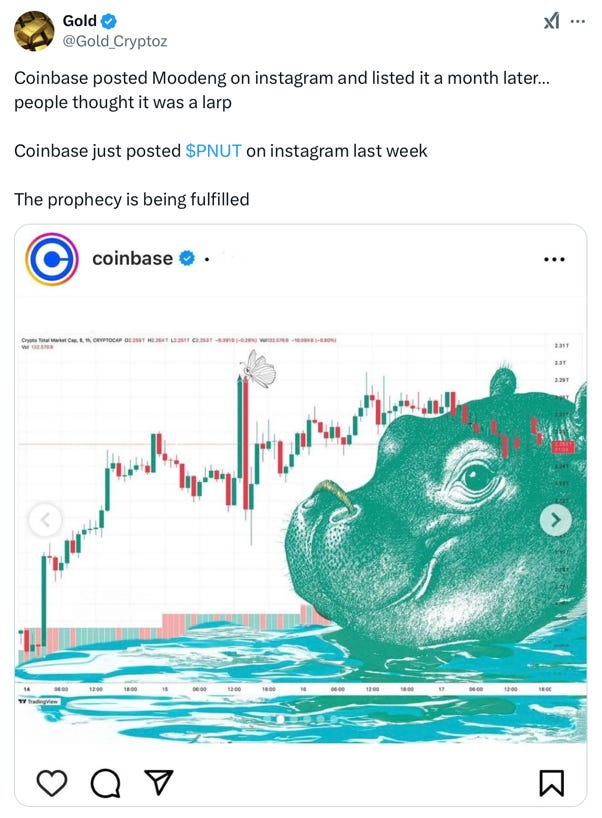

On December 2nd, 2024, one of the largest crypto exchanges, Coinbase, announced that they would list a token called $Moodeng. Listing announcements of tokens almost always result in an increase in the price of the token, since traders know that once the token is listed on Coinbase, more people will be able to buy it. Therefore, $Moodeng increased in price. However, my trade did not have to do with $Moodeng. Instead, just a few minutes after the listing announcement of $Moodeng was released, I saw the following tweet:

Figure 22: Gold_Cryptoz Twitter Post on Speculation of a $PNUT Coinbase Listing

Coinbase had posted the symbol of $Moodeng – a hippo – a month before they announced the listing of $Moodeng. Furthermore, Coinbase had just recently posted a squirrel on Instagram, in the same fashion that they had posted the hippo. The squirrel is the symbol of a prominent memecoin called ‘PNUT the Squirrel’, going by the ticker symbol $PNUT. Thankfully, I was quite early to learn this fact, which I knew would spark rumors that Coinbase might list $PNUT as well. In fact, Coinbase had often listed two similar tokens on the same day, further strengthening the chance of sparking such a rumor. I realized I was early to find out about this rumor and with the idea that it would spread, I quickly opened a long position in $PNUT. However, the trade was not based on the expectation that Coinbase would actually list $PNUT. Rather, the expectation was that this rumor would spread, resulting in people, who believed said rumor, buying $PNUT and driving up its price. Furthermore, people buying $PNUT based on this rumor likely waited for an actual listing announcement by Coinbase, meaning they would not sell their $PNUT tokens even once the rumor had already spread.

4.3.2 Outcome

Once the rumor had spread and I saw more people post about it, I closed my long position, since I was not waiting for a listing announcement. In fact, Coinbase did not go on to announce any listing of $PNUT that day. The only reason I was still able to trade this rumor and gain a profit is because, firstly, I was early to buying it before the rumor sufficiently spread, and secondly, I closed my long position once it had spread and enough people believed in an upcoming listing announcement.

5. Conclusion of Inefficiencies in the Crypto Markets

5.1 History

As demonstrated in the strategies and trade examples above, inefficiencies have long persisted in the crypto markets, allowing even non-professional retail traders to profit from them. While it is difficult to find concrete proof of why so many inefficiencies exist or have existed in the crypto markets, one can still speculate why these markets were, and largely still are, so inefficient. As we have seen, the degree of inefficiency in any market is closely tied to the level of competition within it. When crypto trading first gained popularity, these inefficiencies largely stemmed from the lack of institutional presence and, therefore, the lack of highly sophisticated traders with advanced knowledge and tools. The markets were dominated by inexperienced retail traders.

“It’s insane how much one could’ve made back then; (in 2021) coins doing 100x, news trades continuing to go up for hours, even days” -Huma, full-time crypto trader

5.2 Evolution

Due to the entry of more sophisticated traders and the rise of trading platforms and advanced tools, the level of competition among traders has increased, making the game more difficult. Despite these advancements, crypto markets remain far less efficient than traditional markets such as the stock market. This is largely because the proportion of inexperienced retail traders compared to institutions and professionals in crypto still remains significantly higher than in the stock market. These retail participants lack the tools, speed, and correct insights to compete with seasoned traders, thereby leaving inefficiencies that can still be exploited.

5.3 Forecast

Ultimately, the question of whether crypto markets will ever truly be efficient remains.

In the future, one can expect further entry of sophisticated traders who notice the easy opportunities that exist in crypto. Therefore, it can be expected that the markets will become more efficient and harder to trade. However, we believe that good trading opportunities in crypto will persist, even with a higher level of competition. This can partially be attributed to a low level of liquidity in certain sectors of the crypto space. Since sophisticated traders naturally trade with a larger amount of capital, they need better liquidity for their trades to be executed without affecting market prices heavily. Small memecoins such as $PNUT offer lower levels of liquidity, making it impossible for large players to take trades in these coins with size. Institutions and wealthy traders will have to focus on crypto assets with high liquidity such as Bitcoin, Ethereum, and Solana, thereby leaving less liquid coins and sectors in the hands of smaller, mostly less experienced traders. These less liquid sectors will likely remain inefficient and present opportunities for smart traders who are not wealthy yet.

« I think there will always be opportunities in crypto, it’s just the nature of the space. Builders will always be trying new things and new things will always have some inefficiency. There will always be inefficiency where there is less liquidity, just because sharper players tend to have more capital due to being sharper. » -Dipper

For traders willing to adapt and explore new areas in crypto, the crypto markets will likely remain a place of opportunity, although a more challenging one than in their earlier days.

6. References

iHayes, Adam (2024, July 3) Volatility: Meaning in Finance and How It Works With Stocks. Retrieved Aug 17, 2024, from https://www.investopedia.com/terms/v/volatility.asp

iiKolakowski, Mark (2024, August 6) A Brief History of U.S. Bear Markets. Retrieved Dec 18, 2024, from https://www.investopedia.com/a-history-of-bear-markets-4582652

iiiInvestopedia (2022, April 2) Market efficiency explained. Retrieved Jan 25, 2025, from https://www.investopedia.com/terms/m/marketefficiency.asp

ivJournal of Accounting Research (2021, July 29) How is Earnings News Transmitted to Stock Prices? Retrieved Dec 12, 2024, from https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-679X.12394

vSteer, George (2024, October 27) Jump Trading, Virtu and the ‘hidden optical fibre cable’ under an Ohio field. Retrieved Dec 12, 2024, from https://www.ft.com/content/099342e4-cae8-4ac7-86bd-a3f2048065e8

viWorshipXBT (2024, December 14) Interview with WorshipXBT.

viiDipper (2024, December 30) Interview with Dipper.

viiiHayes, Adam (2024, February 9) Futures Contract Definition: Types, Mechanics, and Uses in Trading. Retrieved Jan 2 2025, from https://www.investopedia.com/terms/f/futurescontract.asp

ixHayes, Adam (2024, July 3) Understanding Liquidity and How to Measure It. Retrieved Jan 5, 2025, from https://www.investopedia.com/terms/l/liquidity.asp

xCryptic Woods (2023, November 24) Interview with jaredfromsubway. Retrieved Jan 2, 2025, from https://crypticwoods.com/blog/jaredfromsubway-interview/

xiTrust Wallet (2024, October 16) What are Sandwich Attacks in Defi? Retrieved Jan 2, 2025, from

https://trustwallet.com/blog/what-are-sandwich-attacks-in-defi

Figure 1 (Cover): Tradingview (updated continuosly) Customized Chart. Retrieved Jan 3, 2025, from

https://tradingview.com

Figure 2: Journal of Accounting Research (2021, July 29) Summarized Findings. Compiled Jan 3, 2025, by ChatGPT

Figure 3: Balchunas, Eric (2024, May 20) Twitter Post. Retrieved December 25 2024, from

Figure 4: Tree of Alpha (updated continuously) Customized Chart. Retrieved December 25, 2024, from ‘Tree of Alpha Discord Bot’

Figure 5: PVP Terminal (updated continuously) PVP Terminal Desktop Application Screenshot. Retrieved December 25, 2024

Figure 6: PVP Terminal (updated continuously) PVP Terminal Desktop Application Screenshot. Retrieved December 25, 2024

Figure 7: GCR (2021, May 14) Twitter Post. Retrieved December 25, 2024, from

https://x.com/GiganticRebirth/status/1393131635663572996

Figure 8: GCR (2021, May 14) Twitter Post. Retrieved December 25, 2024, from

https://x.com/GiganticRebirth/status/1393132005114716161

Figure 9: Sadward (updated continuosly) Customized Chart. Retrieved December 25, 2024, from ‘sadward chartbot 2’

Figure 10: Sadward (updated continuosly) Customized Chart. Retrieved December 25, 2024, from ‘sadward chartbot 2’

Figure 11: Excel (Jan 2, 2025) Excel Screenshot.

Figure 12: Excel (Jan 2, 2025) Excel Screenshot.

Figure 13: Dexscreener (updated continuously) wTAO transaction history. Retrieved Jan 2, 2025, from https://dexscreener.com/ethereum/0x2982d3295a0e1a99e6e88ece0e93ffdfc5c761ae

Figure 14: defi_wonderland (updated continuously) MEV Bots Analytics. Retrieved Jan 2, 2025, from https://dune.com/defi_wonderland/mev-bots

Figure 15: Aevo (2023, August 14) Merging Ribbon Into Aevo. Retrieved Jan 3, 2025, from https://aevo.mirror.xyz/WQk7bwQoKYAghBzw8yH5IRoW8YUqaMqLzoVxzBL8ilU

Figure 16: Aevo Discord Server Inquiry

Figure 17: Tradingview (updated continuosly) Customized Chart. Retrieved Jan 3, 2025, from

https://tradingview.com

Figure 18: Trust Wallet (2023, October 4) Twitter Post. Retrieved Jan 5, 2025, from

Figure 19: Tradingview (updated continuously) Customized Chart. Retrieved Jan 5, 2025, from

https://tradingview.com

Figure 20: Trust Wallet Russia (2023, October 16) Twitter Post. Retrieved Jan 5, 2025, from

Figure 21: Tree of Alpha (updated continuously) Customized Chart. Retrieved December 25, 2025, from ‘Tree of Alpha Discord Bot’

Figure 22: Gold_Cryptoz (2024, December 2) Twitter Post. Retrieved Jan 6, 2025, from

volatile (a): A volatile asset’s price can move heavily in either direction over a short period of time. (Investopedia, 2024)i↩︎

shorting (v): Shorting is a way to profit from a price decrease in an asset. One sells an asset at its current price and repurchases it at a lower price, profiting the difference.↩︎

bear market (n): Bear markets are defined as sustained periods of downward trending asset prices. (Investopedia, 2024)ii↩︎

bull market (n): Bull markets are defined as sustained periods of upward trending asset prices.↩︎

longing (v): Longing means buying an asset, thereby making money if the asset increases in price.↩︎

retail trader (n): A retail trader is an individual who trades with their own money, rather than on behalf of an institution. They are considered non-professional market participants.↩︎

market maker (n): A market maker offers to buy (with bids) and sell (with asks) assets from other people in order to keep a small gap between prices and to make trading easier because more contracts are being traded.↩︎

bids and asks (n): A bid is an order to buy a certain amount of contracts at a certain price. Conversely, an ask is an order to sell a certain amount of contracts at a certain price.↩︎

priced in (v): If an event or news is already reflected in the price of an asset, it is already priced in.↩︎

ETF (n): An exchange-traded fund (ETF) is a type of investment fund that is traded on stock exchanges.↩︎

fee switch (n): If a protocol with a cryptocurrency has a fee switch in place, users that are holding the crypto will get a percentage of the fees that the protocol generates. This incentivizes people to buy and hold the cryptocurrency in order to accrue money from fees.↩︎

arbitrage (n): Arbitrage is the practice of buying something in one place and selling it in another place where the price is higher, profiting from the price difference.↩︎

futures contract (n): A futures contract is a legal agreement to buy or sell a particular asset at a specified time in the future. (Investopedia, 2024)viii↩︎

Liquidity (n): Liquidity refers to the ease with which an asset can be converted to cash without affecting its market price. (Investopedia, 2024)ix↩︎

slippage (n): Slippage is the difference between the expected price of a trade (usually the market price) and the price at which the trade is actually executed.↩︎

gas fee (n): A gas fee is a fee paid for every transaction on a blockchain network.↩︎

PNL (n): PNL stands for Profit and Loss, representing the net monetary outcome of trades.↩︎

Banger as usual